AI for radiology: do we need a new platform?

A neutral marketplace as new national infrastructure will speed adoption of AI for UK healthcare

This article represents my personal views and not those of Digital Catapult, NHS Digital or any other organisation.

In a few years time there’ll be lots of AI apps to help with radiology. I don’t mean research studies or clinical trials. I mean apps deployed and approved and working [1]. This is great news: the demand for radiology is growing and there aren’t enough radiologists [2]. Any tool that can prioritise the urgent cases, quickly eliminate the normal scans, highlight abnormal areas in images, help with a second opinion or assist a more junior clinician will be of great value. However it is also worrying news: how on earth will hospitals do separate contracts and integrations with hundreds of AI providers to cover all the different conditions? And how will AI providers contract and integrate with hundreds of hospitals in the UK, and many more globally?

This won’t be an issue if we end up with a small number of giant AI providers. The trouble is, every specific condition requires lengthy data gathering and cleansing, research, clinical trials and pilots. Even the largest multinationals will struggle to tackle hundreds of these in parallel, or buy enough startups. In the medium term we’re likely to have many AI providers, just as we have many apps in app stores. So we may have viz.ai to identify strokes on CT angiogram imaging for stroke teams, Kheiron to detect breast cancer in mammograms during screening, Imagen to spot wrist fractures in x-rays, Google to find signs of diabetic retinopathy in retinal photographs for opthamologists, Aidoc to detect cervical spine fractures in CT scans, Arterys to speed up analysis of cardiac MRI images, Qure.ai to separate normal from abnormal chest x-rays, Zebra Medical to detect compression fractures from CT chest and abdomen scans, to pick just a few examples.

At the moment hospitals expect to keep radiology equipment and software for 7 years or more. Could they buy radiology AI the same way? Not if they want access to the fast moving pipeline of new AI capabilities. Many of today’s radiology AI success stories can trace their lineage to research first demonstrated only 7 years ago: the “AlexNet” image recognition system of 2012 from Alex Krizhevsky and colleagues at the University of Toronto, whose deep convolutional neural network made an enormous leap in image recognition accuracy. It is an example of how much can happen in just a few years. Investment in AI is at record levels around the world, and innovation is still rapid. The health AI solution you implement next year will be supplanted by one the year after, and another the year after that. These won’t be systems you want to hang on to for 7 years — you’ll need an easy way to switch to the best providers, without having to disturb your workflow or re-do integrations.

The good news is that this isn’t the first time the technology industry has encountered the problem of a two-sided marketplace, with many buyers and sellers. These are ideal conditions for new intermediary platform businesses to emerge. We’ve seen it many times before, from eBay and Alibaba to Uber and AirBnB. We can take it for granted that there will be platforms. The question is: which ones will succeed? And which outcome would be optimal for the UK?

Let’s try to predict some likely scenarios.

A hospital could buy all of its AI from a technology company — organisations like Google have strengths across both infrastructure and machine learning. Working with world-class machine learning and software teams should lead to a rapid clinical benefit. However, it will not be easy to swap in different AI providers. The hospital will be locked in to a specific solution, and may still need additional integrations to cover the full range of conditions.

A competing scenario: radiology equipment companies provide AI apps tied to their existing systems. In this model a hospital may be locked in to AI provided by their equipment vendors, or a subset of AI providers who have exclusive deals with them, and may still struggle to easily switch providers to the best of breed, or to ensure they can cover the full range of conditions and imaging modalities. An example is Critical Care Suite from GE working with UCSF, helping radiologists prioritise cases involving collapsed lungs, integrated with a GE X-ray system. HealthSuite Insights from Philips will be a marketplace for AI providers, curated by Philips. Samsung’s S-Detect for Breast is integrated with a Samsung ultrasound scanner, and helps identify lesion boundaries.

Finally, the existing radiology software providers (such as PACS and RIS systems [3]) could provide marketplaces for AI solutions. This is neater from a hospital’s perspective as it is a single point of integration across their entire radiology workload, and more open for AI providers to participate. The Sectra PACS system has a network of additional applications from partners that includes Cercare for lesion volume and location estimation in brain MRIs. The Nuance AI Marketplace leverages their existing radiology reporting and image sharing systems that have a strong position in the US. The EnvoyAI platform, a spinoff of imaging visualisation provider TeraRecon, is a more independent AI marketplace with many integrations across both AI and radiology systems, and provides the best example of the kind of platform we’re discussing.

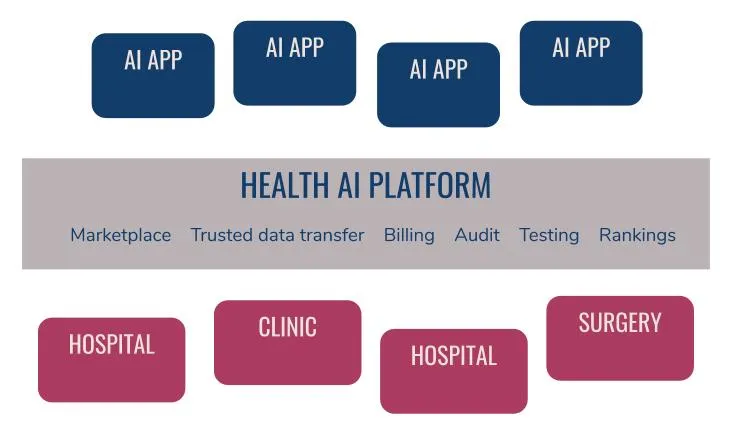

What would be ideal for the UK? A platform that enables rapid innovation, safe trials and tests and ultimately accelerated deployment. I believe there are three core requirements:

- A platform that is open and accessible to any AI provider to easily integrate, test, trial and deploy; to join a marketplace from which hospitals can choose

- A platform that is neutral: neither tied to specific healthcare equipment or software vendors, nor specific AI providers, nor technology infrastructure vendors

- A platform that allows hospitals to easily test AI solutions with their own data, measure performance, switch AI providers as new ones appear on the market, at low cost

As well as those core requirements, we can foresee additional needs that will emerge, and that a platform could provide:

- In the future a regulator ought to insist on a clear audit trail. Which version of an AI system made which prediction for which patient? A neutral platform could maintain such an audit trail. It could even be stored in a distributed ledger like a blockchain to ensure a tamper-proof system.

- A platform seeing the flow of data back and forth would be able to generate synthetic training data for AI providers, staying close to realistic datasets but not including any real personal health data. Speeding access to test data would significantly decrease the development time for new AI systems.

- A platform could ensure secure communication and reliably de-identify radiology scans and reports. AI companies may be newer startups and SMEs, and it will be hard for hospitals to assess their security and privacy practices.

- A platform could maintain rankings of the AI systems and performance indicators that would provide transparency and increase confidence for purchasers, just like app stores show reviews and top charts.

- A platform could track usage for billing and analytics

- New AI apps could shadow existing installations, comparing performance against the same stream of images to see if they are more accurate than incumbents.

- A platform could even allow selection of AI systems transaction by transaction, to optimise costs and performance.

- More sophisticated AI applications may require additional clinical data beyond the transaction of a single radiology session. It would be worth exploring how an AI platform could link at a high level with the national Data Services Platform being developed at NHS Digital.

- Finally, a platform could run continuous re-testing and monitoring of AI applications against hospital test cases. After all, even if the AI system worked when you first tested it, how can you be sure it still works as expected a few months later?

This kind of platform doesn’t do any AI; it provides the infrastructure and plumbing that AI apps will need. It would be a dependable, solidly engineered interface between the complex safety critical systems of hospitals and fast moving AI innovators. Just like the physical infrastructure of roads, railways and bridges, we need digital infrastructure: broadband across the UK; the NHS Digital Spine that already supports information sharing across 23000 healthcare organisations.

We can allow the market to take its course and wait for these platforms to emerge, with a resulting patchwork of independent implementations by different hospitals. But what if we implemented this platform as new national infrastructure. A crazy idea? Perhaps not — it could pay for itself. A simple revenue model would be to charge a small commission, such as $1 per scan [4], for every transaction sent from a hospital to its AI providers via the platform. If the platform succeeded globally it could be a tech unicorn, but even if it played solely in the UK market it could be self sustaining [5].

A platform connecting the UK’s hospitals and healthcare settings with the best of the emerging health AI systems will enable the UK to take the lead in the adoption, deployment and clinical use of AI for healthcare, and open up opportunities for AI innovators. We will be able to safely trial, test and deploy the best AI systems, using a platform that can be sustained through global revenues, while preventing vendor lock-in.

Acknowledgments

The thinking above has benefited from many discussions. It certainly doesn’t represent any sort of consensus as many have been skeptical to say the least! But I’d like to acknowledge the time that people have given up to help think the arguments through, from NHS Digital, NHSX, University Hospitals Coventry and Warwickshire, University of Warwick, Great Ormond Street Hospital, Health Data Research UK, Innovate UK, Digital Health London, Founders Factory, Kheiron Medical, iPlato as well as many individual friends and colleagues especially Chris Gathercole.

Footnotes

¹ As of June 2019 there were 16 FDA approved AI algorithms for radiology. The FDA is actively seeking better ways to deal with algorithms designed to change and improve over time, but for now most AI algorithms are being approved as “de novo” devices (pre-market review for low- to moderate-risk devices for which there is no similar prior device), or have “510(k)” approval (pre-market review where a device is at least as safe and effective as an existing device).

² The Royal College of Radiologists believe the UK’s current shortage is around 1000 radiologists, to keep up with demand without outsourcing, and by 2023 the profession will be 31% understaffed.

³ A picture archiving and communication system (PACS) stores medical images, allowing sharing and viewing, while a radiology information system (RIS) manages the workflow and is the system clinicians use to manage their “reports” (their findings and assessments).

⁴ A handy comparison is the current cost of outsourcing radiology — one provider quotes $4 — $65 per scan depending on the kind of read required. If we guess $20 as a reasonable price for an AI system to charge, then $1 represents a 5% commission for the platform. However the market could be evolve very differently — Zebra Medical are charging $1 per scan across multiple conditions in CT scans, X-rays and mammograms.

⁵ In 2017/18 there were 43M scans in the UK. If in the future 25% of scans use an AI system via a single national platform, even if there is no rise in demand (bear in mind the USA does nearly triple the scans per person), charging $1 per scan results in annual revenues of $10M.